Fidelity to Launch Digital Advice Platform for Advisors

Fidelity to Launch Digital Advice Platform for Advisors

Ever since the launch of Fidelity’s direct-to-consumer digital offering (robo advisor) was announced, I’ve been anxious to see what Fidelity had in store for advisors. The good news for advisors is that the new offering, Fidelity Automated Managed Platform (AMP) was worth waiting for – this joint Fidelity/eMoney development actually leapfrogs the competition.

By deeply integrating Wealthscape features (Fidelity’s next generation advisor workstation) with those of eMoney, Fidelity and eMoney have developed the industry’s first fully-integrated, planning-centric digital advice platform. It is the most impressive advisor-centric digital offering that I’ve seen to date. According to Fidelity, the pilot program is scheduled to begin in the first quarter of 2017. No date has yet been set for the general release.

What makes AMP so impressive? There are many aspects of the offering that I like, but the primary one is the deep integration with eMoney. AMP is not strictly an investment tool as are so many of the competing platforms. Its focus is on three areas:

- Creating goals and tracking progress towards those goals

- Opening and funding accounts to reach those goals

- Helping clients stay on top of their finances in collaboration with their advisor

“We see digital advice as just the latest way eMoney is delivering a solution that evolves how savvy firms and advisors will use automated and integrated technologies to develop their client relationships and scale their businesses into the future, while keeping a planning-centric philosophy at the core”, says Kelly Waltrich, SVP at eMoney.

CAPITALIZING ON INDUSTRY TRENDS

AMP is well suited to capitalize on a number of industry trends. According to a 2015 Gallup Poll (June 29, 2015, Wells Fargo/Gallup Investor and Retirement Optimism Index Survey), modern investors expect an advised experience that looks like the rest of their digital lives. 61% of investors less than 50 years of age and 83% of investors less than 50 years of age rate digital tools as important; and nearly two in three prefer to get advice from both human and digital sources. Furthermore, according to McKinsey & Company, (The Virtual Financial Advisor: Delivering Personalized Advice in the Digital Age), advisors mistakenly underestimate the actual size and growth of the digital market. 40%-45% of affluent consumers who switched their primary wealth management firm in the past 24 months moved to a direct, digitally led firm – in many cases choosing to work with a phone-based advisor at those firms. In addition, according to McKinsey, institutions launching virtual financial advisors have seen a 140% increase in positive customer ratings.

It is worth noting that the winning entry at the recently concluded eMoney Hackathon envisioned some of the features that are incorporated here, including rapid initial goal creation and using the power of the eMoney calculation engine to make some initial goal scenario projections based upon a set of assumptions.

THE AMP EXPERIENCE

Initially, when a prospect logs on, the experience is similar to that of Fidelity GO, the direct-to-consumer offering. Visitors are asked to enter their age and their income. Almost immediately thereafter, the power of the eMoney integration becomes evident. Users are asked if they want to create a retirement goal or another goal. In this example, we’ll confine the discussion to a retirement goal.

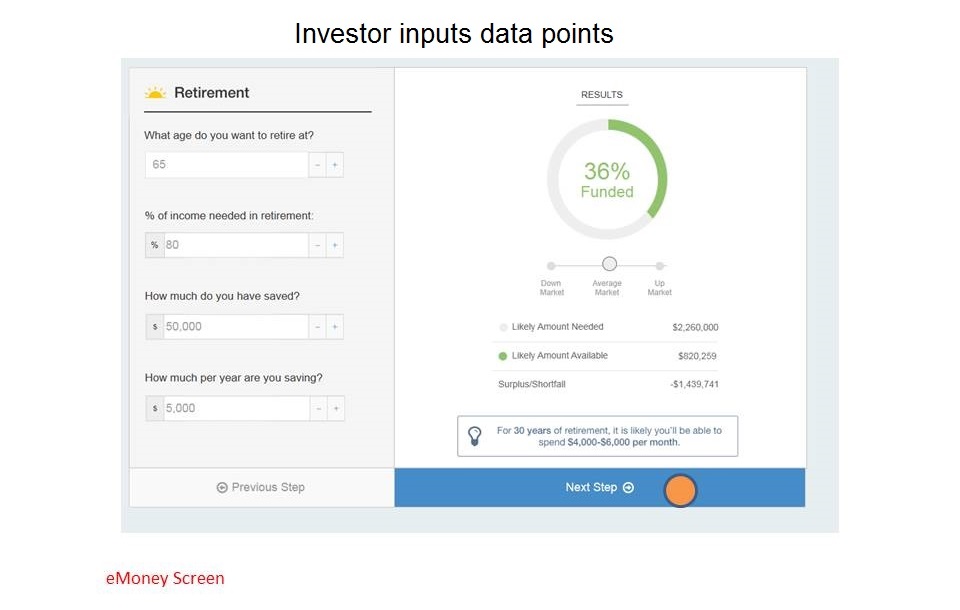

For the retirement goal, eMoney already generates a rough estimate of how much retirement will cost. For the purpose of this example, the estimated retirement cost is $2,260,000. The user can click through to the next page to learn more.

Here we can see some of the assumptions that went into the eMoney projection on the previous screen. It is assumed that the prospect will retire at age 65 on 80% of current income. It is further assumed that the prospect has already saved $50,000 and is currently saving $5,000 per year. As the screen above shows, using the current assumptions, the prospect will only fund 36% of the required funds for retirement given “average” market conditions. The graphic also lets the prospect know that under the current scenario, it is likely that they will only spend between $4,000-$6,000 in monthly income.

The prospect can change any of the four primary inputs easily. This will cause eMoney to recalculate the results almost instantaneously. As the prospect explores retiring later of saving more, they can see immediately the impact on their funding percentage and likely allowable monthly spending. They can also click under the funding chart to see what the impact of above average or below average market returns will do to the scenario. Granted, all of these estimates are only that; they are estimates based upon a number of behind the scene assumptions that cannot be altered by the user (longevity, SS assumptions, etc.) because the application is only requiring minimal inputs at this time, however they are an excellent staring point.

Assuming that the prospect wants to proceed, they can then choose to open either a tax deferred account or a taxable account to fund the savings gap. The next step is to complete the risk questionnaire.

The risk questionnaire is totally customizable. Independent RIA firms and broker/dealers can use the template provided, or they can create their own questions. Whether they use the template or build their own, advisors can map the scores to a portfolio.

As is the case with Fidelity GO, the investment models are created by Geode Capital Management. Fourteen models are available to advisor, seven that are designed for taxable accounts, and seven for tax-deferred accounts. The portfolios all make use of low cost ETF’s. I’m told that the underlying ETF fees on the portfolios average below 15 bp. According to Fidelity, the portfolios are tactically managed, and they are managed with an eye to tax sensitivity as well. In effect, the advisor is hiring Geode as a subadvisor, and the advisory firm or B/D maps portfolios to risk scores.

After the prospect completes the risk questionnaire, a recommended portfolio is suggested. eMoney generates a graph that shows a range of estimated future returns for the portfolio selected. The prospect can click on other models to see what their range of future returns is estimated to be.

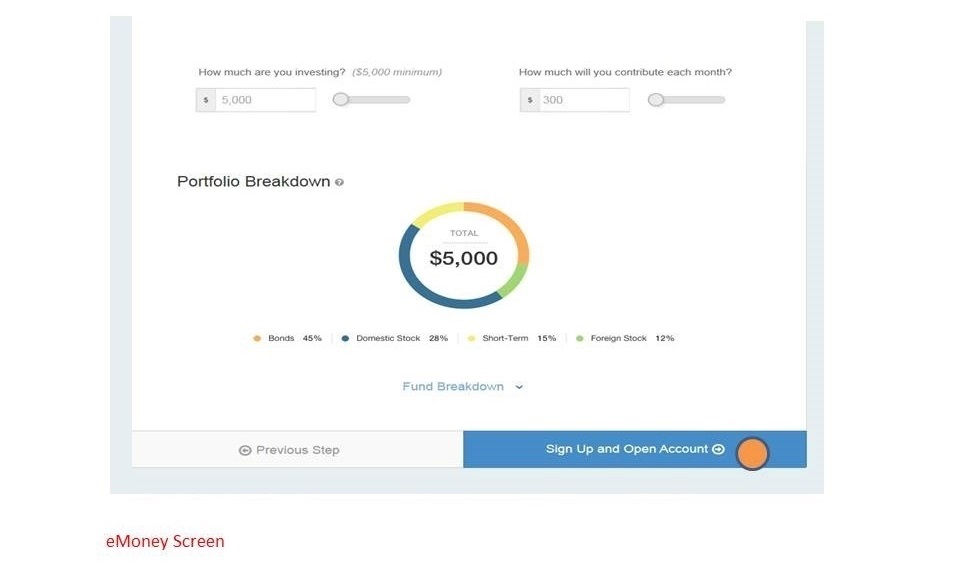

Prospect Can Change Investments or Contributions, View Portfolio Breakdown

The prospect can then choose to implement. On the following screen, they can change the initial investment amount and/or change the monthly contribution. The can view the portfolio breakdown by asset class, and they can click through to see the actual ETF portfolio to be implemented.

The next step entails signing up with eMoney. The user creates a log-in name and password, answers security questions, and agrees to terms of service. Next, the prospect goes through the digital, online account opening process. This includes the signing of the advisor’s digital investment advisory agreement.

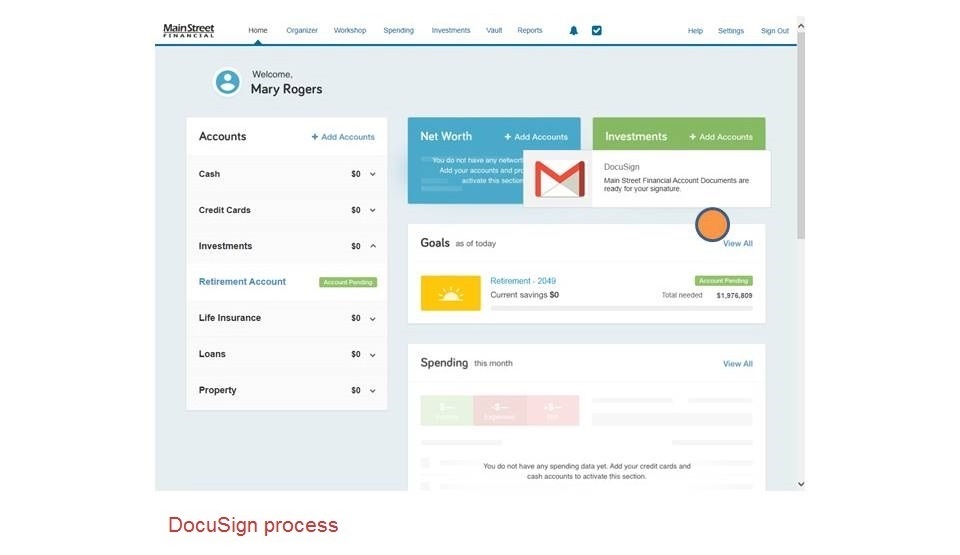

Email begins DocuSign Process

As we can see in the illustration above, the prospect is already logged in to the client portal powered by eMoney. Under the account heading, we see that a retirement account is pending. An email arrives in the prospect’s email account that triggers the DocuSign process. The prospect clicks on the email and electronically signs the required documents. A button then appears next to the retirement account that says “fund account.” The new client then presses the button and establishes a link with a bank account to fund the AMP account (accounts can also be funded through an ACAT transfer of assets). Bank account linking takes place in near real time.

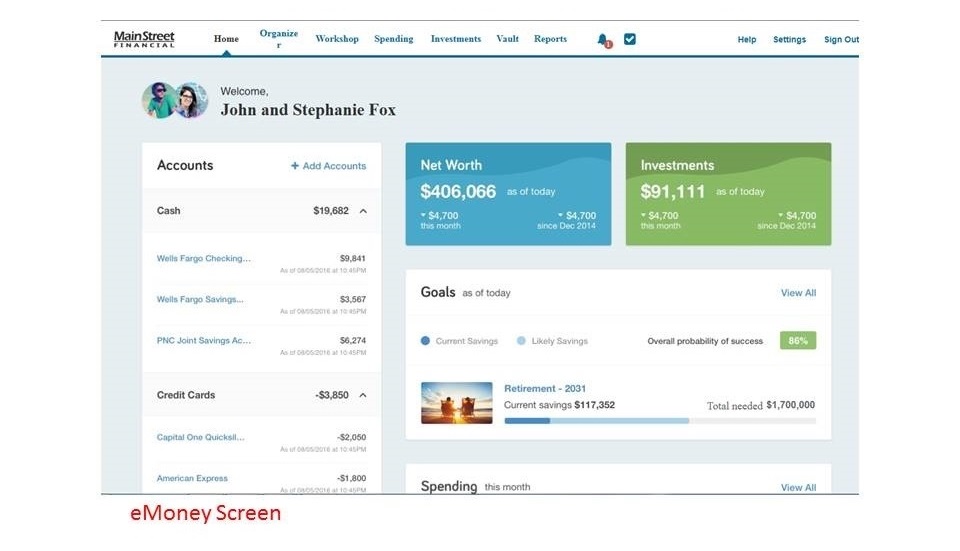

The client can then make use of the eMoney portal aggregation features to link and view all of their financial accounts. The portal will then display accounts, goals, alerts, spending and much more.

eMoney Client Portal with Aggregated Assets, Alerts, Goals, Net Worth, Investments Spending and More

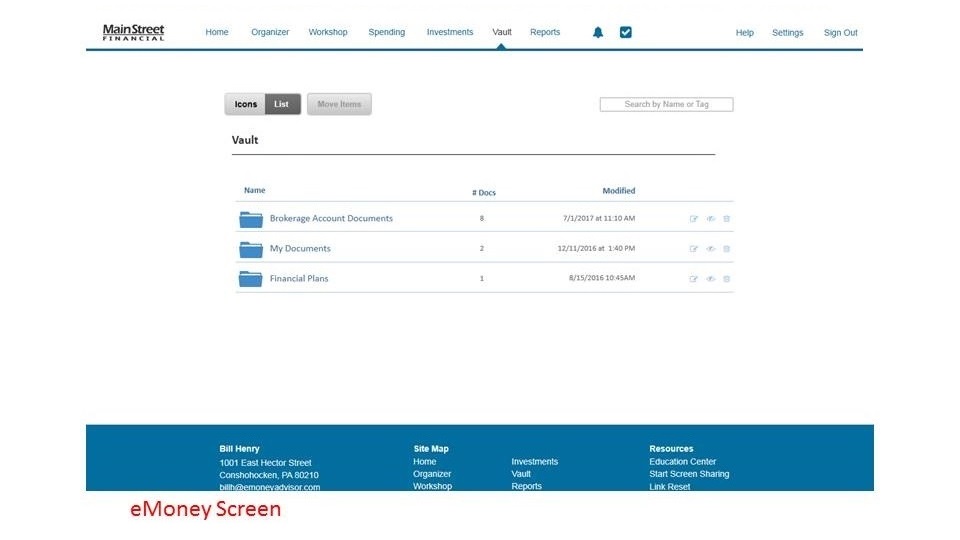

Through the Fidelity integration, all brokerage documents (statements, trade confirms, tax documents) will be available in the client vault.

Client Vault

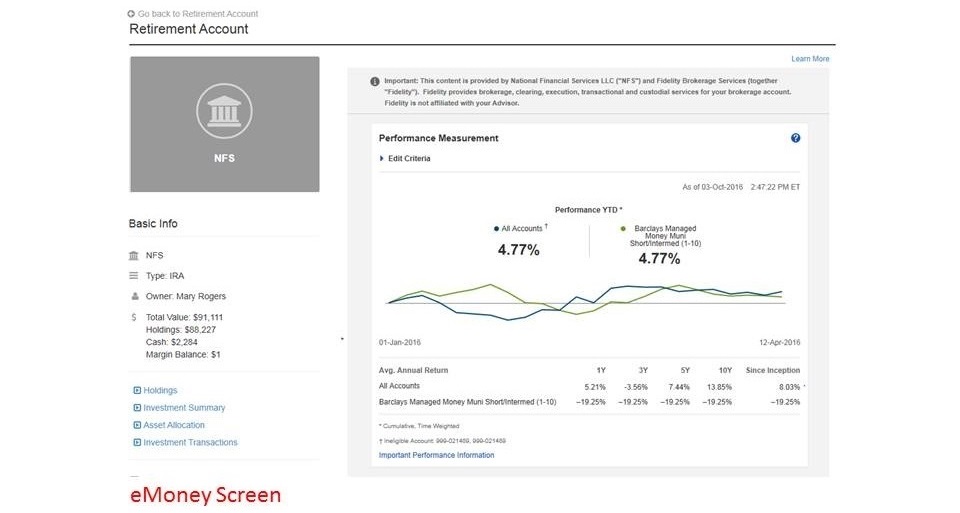

At the launch of AMP, performance reporting for the AMP accounts will be available, powered by Fidelity’s new performance reporting engine. The longer term plan is to allow the performance engine to calculate performance for all accounts aggregated here, but that feature will not be available in the initial version.

Performance Reporting Powered by Fidelity, Displayed in the eMoney Portal

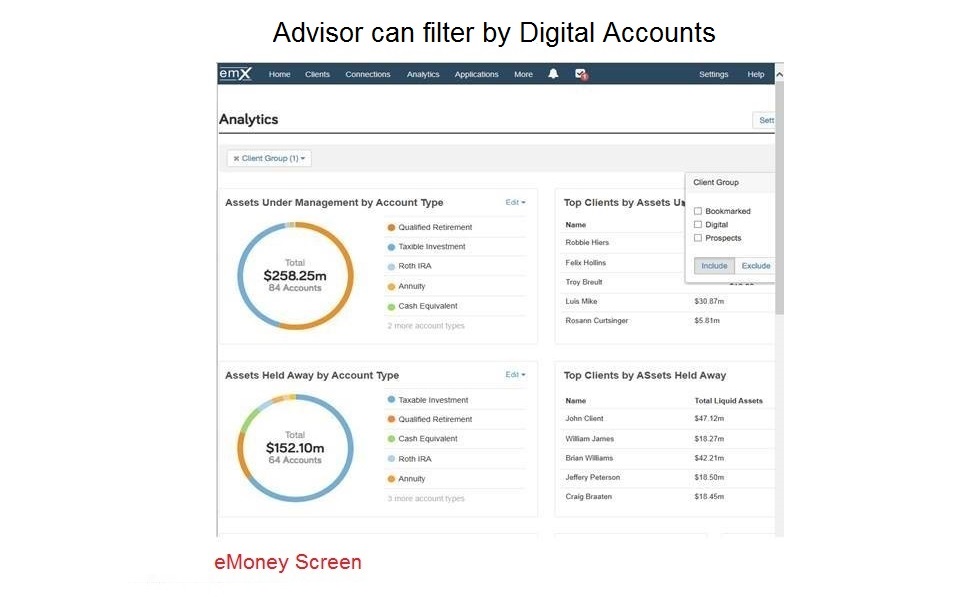

The advisor can view all of the clients’ accounts, both managed and held-away. These accounts can be filtered by the advisor for analysis.

I very much like the prospect’s ability to try different scenarios without committing to anything initially. Although eMoney has to make a lot of assumptions given the space initial data collected, the projections are still very helpful as a starting point. There is plenty of time to refine the plan later should the client choose to fully engage with the advisor.

The true straight-through digital onboarding is a welcome addition. Hopefully Fidelity will soon extend this capability to all advisor account openings. The integrated performance reporting powered by Fidelity, the future projections powered by eMoney, and access to the full eMoney client portal experience for the end-user are all great features, as are the built-in billing capabilities.

Rolling out AMP is easy. You can link it to your existing website (see example below), create a unique landing page, or create social media hooks to drive traffic to your offering.

The ability to seamlessly transition clients from an AMP relationship to a full eMoney financial planning relationship and/or Fidelity custodial relationship is another highly-attractive feature.

Existing eMoney clients will have access to AMP by simply turning it on once it is available. Other advisors will need to purchase at least the lowest-cost eMoney offering, emX Select, which includes the Applications Dashboard, Aggregation Engine, Advisor Dashboard and Client Portal, without financial planning capabilities. For most advisors, the price of Select is in the $1,500-$1,800 per year range, depending upon discounts available.

The pricing for AMP technology has not yet been finalized. The folks at Fidelity have indicated that they are well aware of what competitors charge, and that they intend to be competitive. My best estimate is that pricing will fall between 10-20 bps initially.

Although AMP is very impressive, there are a few things that would make it even better. I am sure that some advisors would like the ability to create their own portfolios of ETF’s. This option is not currently available. You have to use the Geode portfolios. I suspect that if there is sufficient demand, Fidelity will allow advisors and institutions to create their own in the future.

It also occurs to me that many independent RIAs and institutions now use a risk tool such as Riskalyze or Finametrica, and that they would like the ability to use one of these tools in conjunction with AMP. Currently, such integrations do not exist. I suspect that Fidelity will receive numerous requests to include these integrations in the near future.

As stated earlier, advisors are sure to want performance numbers for all accounts aggregated in the client portal. One would think that the incremental cost to Fidelity of calculating performance for all accounts custodied at Fidelity would be minimal, so I’d expect that feature to be added soon. I’d assume there will be a more substantial cost for providing performance numbers on held-away accounts, so if that feature is added, an additional charge might be necessary.

Although the AMP platform is impressive, perhaps the most significant aspect of this initial eMoney/Fidelity collaboration is that it displays the true potential of the combined firms. Many advisors and commentators initially feared that Fidelity’s purchase of eMoney would restrict the distribution of eMoney technology in the future. They could not envision how combining the intellectual properties of both firms might actually expand their joint market share and provide benefits to the advisor community. Now that we are beginning to see the fruits of their combined labors, it is apparent to me at least that both eMoney clients and Fidelity clients will benefit from the collaboration of these two firms.

{kind=link}

{kind=link}